Valuation

Valuation is a key factor when investing. This consists of finding out if the price paid for a share or asset in general is correct in relation to the future flows that that business can bring us. Or seen from another point, it tells us how many times the market is willing to pay for a company, in relation to its future profits, at a given present moment. This is why paying very high valuation multiples in some cases (overvalued companies) can distance us too much from reality and force us to overpay prices, even for good companies. For this reason, valuing correct and conservative multiples is essential.

Valuation consists of numbers, but also (real) stories. It's no use doing numbers without knowing the story behind a business. The story is extremely important, and consists of everything that is behind the company and that is not quantifiable. In bubbles there are usually numbers based on (unreal) or overstated stories that lead to poorly made numbers and therefore bad valuations. Or what is even worse, history without numbers (smoke), buying companies based on a brilliant idea but that will never happen because they are not supported by something solid.

In terms of valuation, there are two methods generally used by investors:

(1) Valuation by Multiples and

(2) Discounted Cash Flow Valuation.

Valuation by multiples is the method commonly used by value investors as it is best suited to compare companies, especially in the same sector.

(1) Valuation by multiples: This method consists of estimating the value of a company based on future business profits, applying multiples we obtain the future value, we bring it to the present and compare it with the current market value, if our result is lower. , we will be buying at a good price. It is necessary to know the multiples of the sector and the historical of the company to try to buy at low multiples, quality companies good businesses in this way we make sure that we are "not" overpaying for the euphoria and excesses of the market (main cause of bad returns). in a bag).

Multiples is something that usually causes a lot of mystery when you start to analyze companies, and the question is, at what multiples do you value a company? There are some valuation ranges, there are general ones and other sectorial ones, in relation to the sector and characteristics of the business, this is something that we must know to obtain a correct valuation.

« In general terms, on average, the market grows at 8% and multiples of 15x PER and 11x EV/EBITDA »

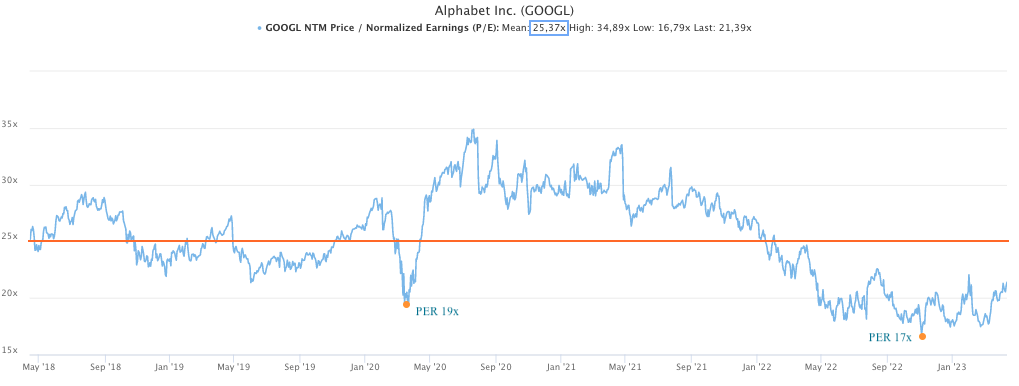

The good students in the class like Alphabet (GOOGL), grows on average between 15%~20% and we could apply higher multiples of 25x PER and 16x EV/EBITDA for its valuation. The following graph from Alphabet shows the valuation of the company from May 2018 until May 2023, a company of high quality and competitive advantage. In the last 5 years, Google has effectively traded at PER 25x on average, but in specific situations of market panic, such as in March 2020, or since the outbreak of the Russia~Ukraine war in May 2022, valuations have reached multiples. below PER 20x. Absolutely nothing has happened to the company in all this time, quite the contrary, it continues to grow and its earnings per share (EPS) have gone from $2.19 to $4.56 more than double in the same period of time. It was certainly a good time to invest in the company in March 2020, and it is now too.

¨ If we estimate that Alphabet will have earnings per share (EPS) of $7 in three years in the future, at a multiple of 25x PER, we get a price target of $175 and currently Google is trading at just $100. We are buying the company at a 43% discount. This only happens on the stock market "

Alphabet valuation by PER

This is a simplified way of how to carry out the valuation of a company, obviously it is a bit more complex and other points must be analyzed, in this way, we will be able to obtain a more accurate result.

(2) The cash flow discount method presents certain problems that make it impractical from the point of view of an investor in companies. Because investing in the stock market has many moving parts, and the market is not perfect, the DCF discounted cash flow method is less widely used. The DFC applies very well in investments where future cash flows are foreseeable, in the construction of a bridge or a highway where a return can be estimated in advance in relation to the years of useful life of these infrastructures. But when valuing companies, the information is not always perfect or complete, future sales plans change, as well as strategic plans, in addition to various external factors such as inflation, raw material prices, etc. It is this subjectivity and uncertainty regarding the calculation of the current value of the company through the DCF method, which invites analysts to make use of comparables through the valuation multiples method.

Overall index valuation

At a general level, the Standard & Poor's 500 (S&P 500) index, the most representative index of the US stock market, also trades at certain multiples in relation to the benefits. Historically, it has traded at 15x PER multiples on average. In moments of euphoria such as in the year 2000, during the dot-com bubble, or in 2021 during the post-covid euphoria, valuations reached levels above 30x, these are undoubtedly the highest valuations since the crash of 1929 where the people previous months were euphoric, anything went. These excessive valuations on the stock market are a clear sign to be cautious and reduce position, have waited for the market euphoria to calm down and return to normal valuations, and once again expand position.

The chart below shows the historical PER of the S&P 500 from 1870 to 2020. In all bubbles, valuations have been well above average, reaching multiples of over 30x. The valuation peaks correspond to the months prior to the 1929 crash, the 1999 dotcom bubble with the subsequent crash in the 2000s and the recent post-covid bubble in 2021, to end up falling by more than 20% in 2022.

S&P 500 PE Ratio historical

Evidently, investment is a complex world, multiple variables interact, where one must think about how well the company will do it and, on the other hand, how the market will react with depressive or euphoric moods, and it is at these points, where valuation multiples play an important role.

In other words, the valuation of a stock may be depressed and move the price down, but absolutely nothing happens to the company, the fundamentals grow year after year, increase sales, EBIT margin expansion, profit, FCF, etc. and the market "says otherwise" ¨, until at some point the stock market agrees with us (expansion of multiples) and puts the stock in price. ¨But for this, many times you have to know how to wait.¨

The PER ratio is not the only way to obtain a valuation, there are other equally valid ratios, depending on the financial situation and sector of the company. Some of these ratios are P/FCF, EV/EBITDA, EV/EBIT among others.

¨Shares have a true or fundamental value, different from their market value. The fundamental value of a stock can be defined as the relationship between the underlying assets and their ability to produce earnings; and the market price of a stock is supposed to trend towards its fundamental value, but at the same time the market price is influenced by mister market's feelings of euphoria or depression.